The Scottsdale and Phoenix Real Estate Market: April 2026

Spring arrived with more supply than expected, softer pricing at the top end, and buyers who are still showing up but taking their time. The April data from ARMLS and Realtor.com tells a fairly consistent story across both local and national markets: sellers who understand current conditions are transacting, and those who are not are sitting.

For Scottsdale and Paradise Valley specifically, there is more nuance worth unpacking.

National Housing Market Snapshot

April opened against a rough backdrop. Mortgage rates had been climbing for five straight weeks and hit a seven-month high of 6.46% on April 2. Consumer sentiment was down, inflation was running at 3.3%, and the broader economic picture looked uncertain. The expectation was that the spring market would stall.

It largely did not. Rates pulled back through the rest of the month, finishing below 6.30%. National new listings reached their highest April volume since 2022, up 8.7% month over month and 1.1% year over year. Pending sales rose 1.0% year over year, marking the fourth consecutive month of year-over-year growth. Contract cancellations tracked below last year. Active inventory nationally crossed one million listings for the first time in years, reaching 1,002,935, though that figure remains roughly 12.5% below pre-pandemic norms.

The more interesting signal is in how sellers are behaving. The national median list price fell 1.4% year over year to $425,000, its sixth consecutive monthly decline. And price cuts also fell compared to last year, with 16.7% of listings seeing a reduction versus 17.9% in April 2025. That combination suggests sellers are entering the market with more realistic expectations rather than testing high and adjusting later. It is a meaningful shift in seller psychology from 2024 and early 2025.

Time on market nationally was 52 days, up two days from last year. Not dramatic. But it is the 25th consecutive month of homes taking longer to sell on a year-over-year basis. That trend has not reversed.

“Sellers appear to be adjusting expectations before listing rather than after. That shift in how properties are being priced is more significant than the headline number.”

What Happened in Arizona This Month

The Phoenix metro remains one of the more active markets in the country, but April data from ARMLS reveals a market in the middle of a rebalancing rather than one with clear directional momentum.

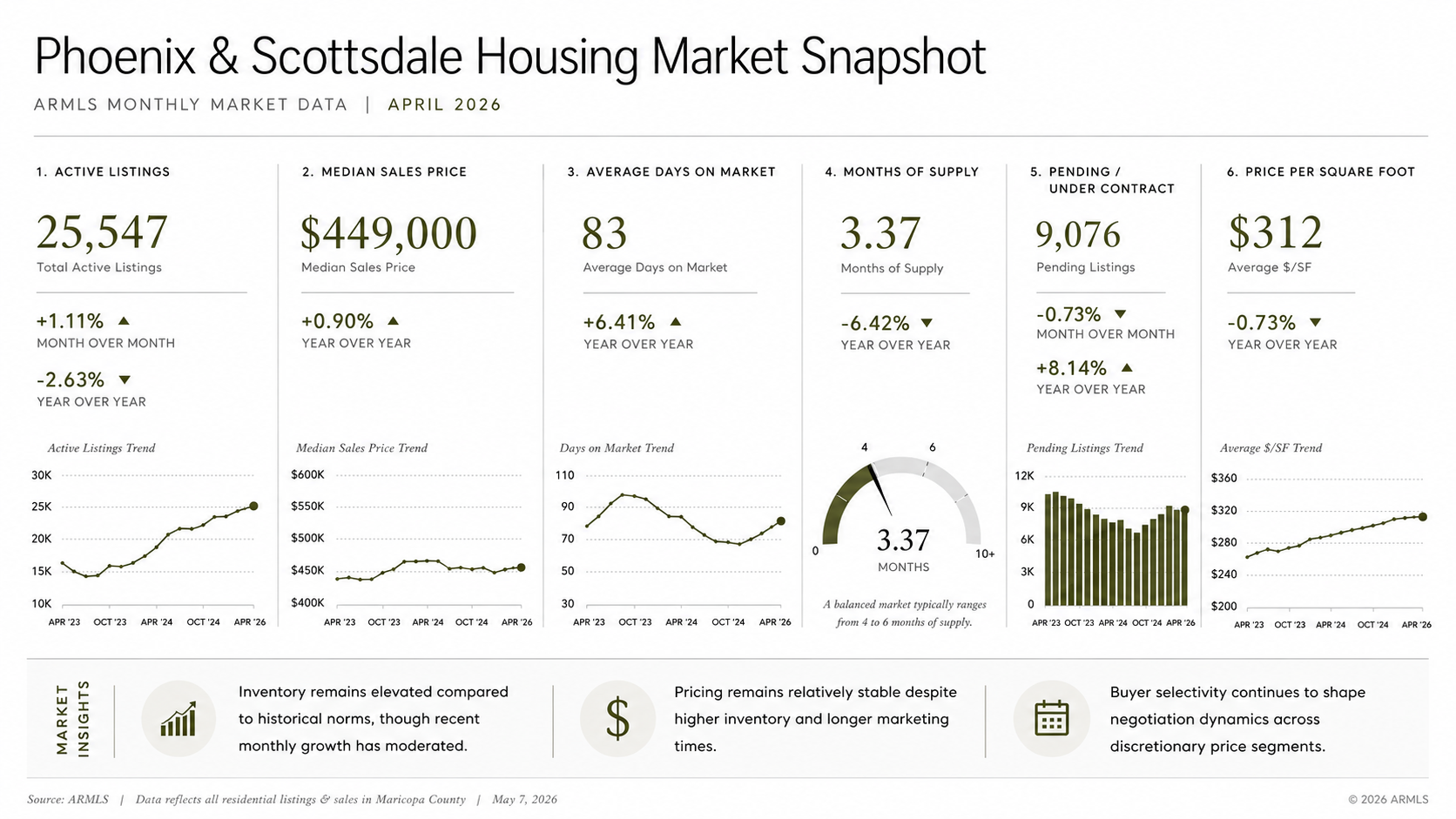

Active listings (excluding under contract) rose to 25,547, up 1.1% from the prior month and 4.85% from three months ago. That is meaningful supply expansion from the winter floor, though still slightly below the same period last year. Absorption currently sits at 29.67%, with months of supply at 3.37. Both numbers point to a market that is not oversupplied, but also one where sellers no longer have the leverage they held in 2022 and 2023.

Sold listings for April came in at 7,581, essentially flat with the prior month (7,568) and up about 4% from a year ago. Average sale price came in at $599,310, down 6.08% from March's $638,076. Median sale price was $449,000, down modestly from $455,000 the month prior. Days on market averaged 83 days across all sold properties, with a median of 55. Both figures have improved substantially over the past three months, when average DOM was sitting at 94 days.

New listings came in at 10,494, down 3.4% from March but up 2.76% from six months ago. The average list price for new inventory dropped to $679,379 from $684,289 the month prior, and sits significantly below the $739,695 average seen three months ago. That pullback in new list prices reflects sellers recalibrating rather than overreaching.

Price per square foot on sold listings averaged $279.69, down from $283.92 in March. Median price per square foot was $254.52, nearly flat. Over a 12-month comparison, median price per square foot is down about 1.26%. Prices are not collapsing, but they are not appreciating either.

Scottsdale and Paradise Valley: Reading Between the Lines

The metro-wide ARMLS data includes everything from entry-level Phoenix condos to Paradise Valley estates. The Scottsdale and PV luxury segment behaves somewhat differently, and April reinforced a few patterns worth watching.

Realtor.com's data shows the Phoenix-Mesa-Chandler metro recorded a 29.1% price cut share in April, with median list prices down 5.0% year over year. Those figures are influenced heavily by mid-market inventory. In the luxury segment above $1.5M, the dynamics are more selective. Well-presented properties in established neighborhoods are still generating serious buyer interest. Properties that came to market overpriced relative to recent comparables are sitting.

The gap between aspirational pricing and market-supported pricing has been widening since late 2025. Buyers above $1M are doing more due diligence before committing and are less likely to overlook condition issues or location compromises. That is not pessimism. It is selectivity. The buyers are there. They are just not in a hurry.

Paradise Valley in particular has seen constrained new inventory. What is coming to market tends to be either priced correctly and moving within 30 to 60 days, or overpriced and sitting well beyond that. Sellers who are working from 2023 comparable data are finding themselves ahead of where buyers are willing to go in 2026. The adjustment period on those properties tends to be expensive in both time and eventual concessions.

Arcadia and Arcadia Lite continue to hold up relatively well. Demand from move-up buyers and out-of-state relocators remains more consistent in that corridor than in some outer Scottsdale zip codes. Inventory is tighter there, and that compressed supply is keeping prices steadier.

Cody Wolfe: Expert Insight

“The homes generating activity right now are the ones that came to market already aligned with where buyers are. Sellers who price for last year’s market are not losing offers, they are not seeing tours. The miss happens before anyone writes anything.”

What Buyers and Sellers Should Watch Next

A few things to keep an eye on heading into May and early summer.

Mortgage rates are the obvious one. The current range of 6.30% to 6.46% is meaningfully better than the 7.17% buyers were facing in April 2024. That context matters. Each rate move has an outsized effect on monthly payment sensitivity at the price points common in Scottsdale and Paradise Valley. Any sustained move below 6.0% would likely accelerate buyer activity notably.

Inventory management will also matter. The surge in new listings nationally, particularly in the Northeast and Midwest, has started to soften those constrained markets. Arizona's inventory picture is more stable. Months of supply at 3.37 is not alarming, but it does give buyers more options than they had 18 months ago. If new listings continue coming in around 10,000 to 11,000 per month through the summer, absorption will be the variable to watch.

Seller behavior locally is starting to shift in a constructive direction. Average list prices on new inventory are coming down while median list prices hold closer to stable. That pattern, similar to what Realtor.com observed nationally, suggests sellers are entering negotiations from a more realistic starting point. That tends to produce more transactions, which benefits both sides.

For luxury buyers specifically, the spring window is real. Fewer competing buyers than 2022 and 2023, more selection, and sellers who are negotiable on terms if not always on price. The combination is actually quite favorable for well-prepared buyers who know what they want.

Final Thoughts

April 2026 was not a dramatic month in either direction. The market held. Buyers and sellers are transacting at a pace that reflects new normal conditions rather than the frenzy of earlier years or the standoff of 2023.

The most consistent theme across both the national data and local ARMLS numbers is that accuracy matters more than ever. Accurate pricing from sellers. Accurate market reading from buyers. Properties positioned correctly for today's conditions are moving. The ones that are not are waiting for a market that may not return.

If you want a more detailed breakdown of your specific neighborhood, property type, or price point, reach out directly.

FAQs

Q: Is the Scottsdale real estate market a buyer's or seller's market in 2026?

A: The Phoenix-Scottsdale metro is in balanced to slightly buyer-favoring territory as of April 2026, with 3.37 months of supply and 25,547 active listings. Sellers retain leverage in well-located and well-priced properties, particularly in Arcadia and Paradise Valley, but buyers have more options and time than in recent years.

Q: Are home prices falling in Scottsdale?

A: Median sale prices in the greater Phoenix metro are slightly softer year over year, with the April 2026 median coming in at $449,000, down modestly from the prior month. Price per square foot is also down about 1.26% over the past 12 months. The luxury segment above $1.5M is holding more stable in established neighborhoods like Paradise Valley and Arcadia.

Q: How long are homes sitting on the market in Phoenix and Scottsdale?

A: Average days on market for sold properties in April 2026 was 83 days, with a median of 55 days. Both figures have improved from the winter peak of 94 average days. Well-priced homes in high-demand areas are moving considerably faster.

Q: What is the mortgage rate environment like for buyers in spring 2026?

A: Rates peaked at 6.46% on April 2 and pulled back to just below 6.30% by month-end. While higher than late 2025, rates are meaningfully below the 7.17% buyers faced in April 2024, which is relevant context for affordability calculations.

Q: Is Paradise Valley real estate a good investment in 2026?

A: Paradise Valley continues to hold its value relative to broader metro trends, with constrained inventory and consistent demand from high-net-worth buyers. Properties priced accurately relative to recent comparables are transacting. The market rewards preparation and positioning more than it did in prior years.

Cody Wolfe is a luxury real estate agent and Partner at The Agency Scottsdale, specializing in Old Town, Paradise Valley, and McCormick Ranch.